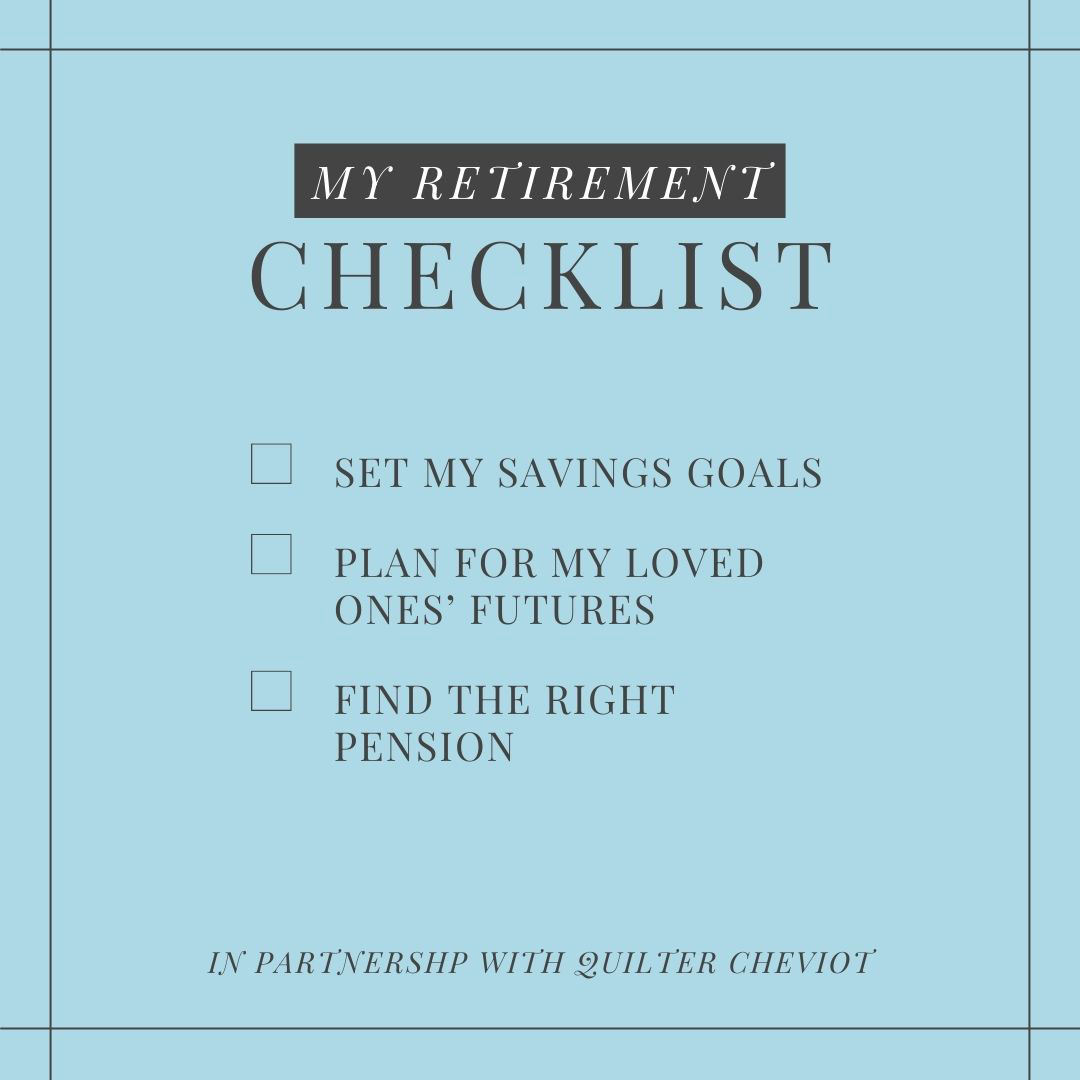

This Retirement Checklist Lays Out 3 Steps To Success

By

2 years ago

Plan for tomorrow, today.

Don’t leave it too late to start thinking about your retirement. Studies indicate over 60% of pensioners who pay income tax could be £650 worse off annually by 2027. Pair this with rising inflation, and many are forced to spend more to maintain their lifestyle. Withdrawing more money can lead to the unsettling prospect of outliving your savings, and the need to adjust one’s standard of living.

That’s the bad news. The good news is that there are measures you can take to prevent these concerns later down the line. This handy retirement checklist by the experts at Quilter Cheviot lays out some of the things to consider to help ensure your retirement is just as you had envisioned it. You can also download your complimentary full Retirement Report.

Your Retirement Checklist

These are the top three questions you can ask yourself today to start planning for your retirement.

1. Am I Saving Enough?

The World Economic Forum recommends setting aside 10 to 15% of your annual income for retirement. Unfortunately, many fall short of this goal. And with rising inflation, it’s tempting to redirect funds to meet immediate living expenses, leaving retirement plans underfunded.

Inflation’s impact on future planning is often underestimated. A 50-year-old with a £100,000 annual income supporting their lifestyle will need an income of £180,000 in 15 years’ time to maintain a similar standard of living based on expected inflation – that’s an increase of 80%.

When preparing for retirement, consider the 4% rule: a retiree should withdraw 4% of their retirement savings in the first-year post-retirement, and withdraw the same amount – adjusting for inflation – every year thereafter. This way, you’ll maintain a steady stream of funds without completely depleting your resources.

2. What Do I Want To Leave Behind?

Your retirement pot can go so much further than you think. It’s not only a tool for sustaining a post-retirement lifestyle; it’s also an instrument to enhance the inheritance you leave your loved ones.

Unfortunately, many lose a significant part of this wealth once it reaches the Inheritance Tax (IHT) threshold, currently set to £325,000 until at least 5 April 2028. This means any amount above £325,000 could be taxed at 40%.

To ensure your wealth effectively benefits your family’s future as it has supported you, it’s essential to understand how to use various reliefs, allowances, and exemptions. Strategic planning can help preserve your wealth for your loved ones, mitigating the impact of IHT.

3. Have I Got The Right Pension?

Defined benefit pensions; defined contributions pensions; cash flow modelling; retirement income strategies; ISAs: there are numerous routes that you can choose when deciding what retirement strategy would work for you.

It’s a landscape that can prove overwhelming, which is where the expertise of a specialised Financial Planner becomes invaluable. They can assess your current financial standing, your aspirations, and your necessities to devise a retirement strategy that aligns with the lifestyle you desire, both before and after retirement.

Want To Know More?

This is only the tip of the iceberg when it comes to retirement planning. There is so much more that can help you ensure your later years are just how you envision them.

Quilter Cheviot is here to help with their full retirement report; a one-stop shop for everything you need to plan for a successful retirement. To get your very own copy, click here.